Annuity Payment

The above estimate and other rates on this website are based on Go2Income market-based pricing methodology assuming source of premiums are non-qualified savings. For a Current Annuity Quote and information for qualified savings Talk to a Specialist.

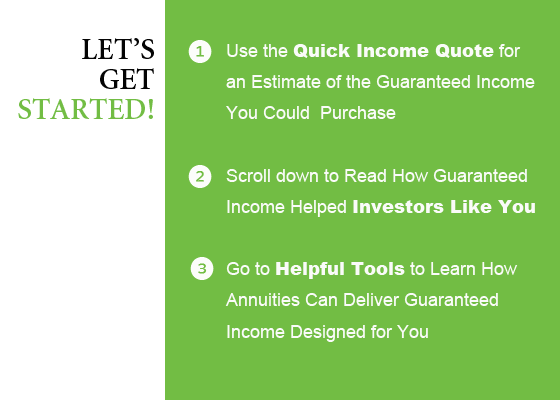

Design Your Own Annuity.

Understand How Your Annuity Works.

Compare Your Annuity to Other Annuities.

?

Request a Personalized Go2Income Guide to Selecting Your Annuity.